In today’s digital age, electronic payments have become increasingly popular and convenient. One such method is the ACH transfer, which stands for Automated Clearing House. Automated Clearing House (ACH) transfers allow individuals and businesses to send and receive funds electronically, providing a secure and efficient alternative to traditional paper checks.

In this comprehensive guide, we will delve into the world of ACH transfers, exploring how they work, their benefits, limitations, and much more.

How Does an ACH Transfer Work? Exploring the Process Step by Step

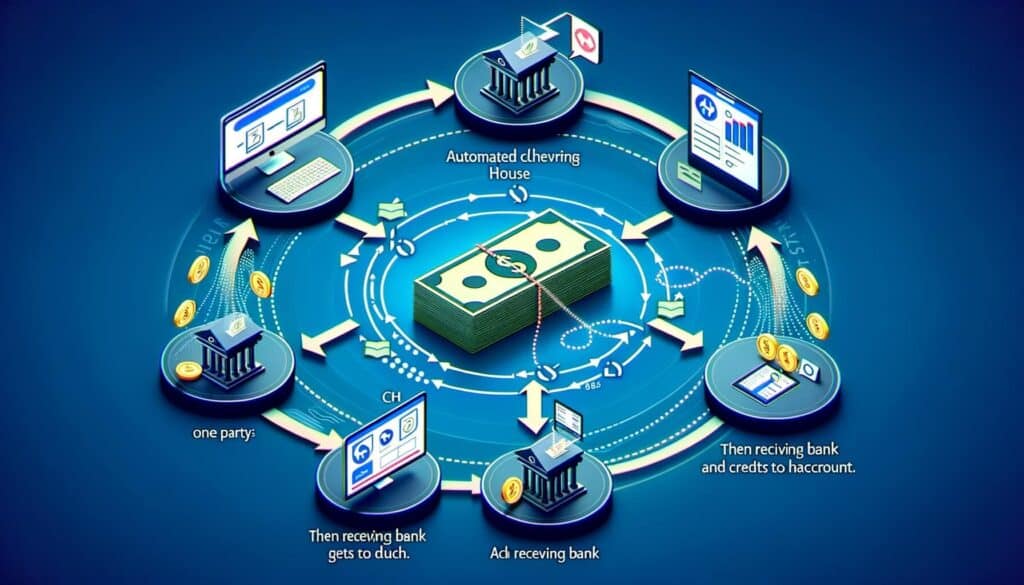

ACH transfers involve the movement of funds between two bank accounts through the Automated Clearing House network. This network acts as a central clearinghouse for electronic transactions, facilitating the transfer of funds between financial institutions. The process can be broken down into several steps.

Step 1: Initiation

The sender initiates an Automated Clearing House (ACH) transfer by providing their bank with the necessary information, including the recipient’s bank account number, routing number, and the amount to be transferred. This information can be provided through various channels, such as online banking platforms or mobile applications.

Step 2: Authorization

Once the transfer request is received, the sender’s bank verifies the availability of funds in the sender’s account. If the funds are available, the bank authorizes the transfer and sends the request to the ACH network.

Step 3: ACH Network Processing

The ACH network processes the transfer request, ensuring that all necessary information is included and that the transaction meets the required standards. This includes verifying the accuracy of the routing and account numbers, as well as checking for any potential fraud or errors.

Step 4: Clearing and Settlement

After processing, the ACH network sends the transfer request to the recipient’s bank. The recipient’s bank then credits the funds to the recipient’s account. This process typically takes one to two business days, although it can vary depending on the banks involved.

ACH Transfer vs. Wire Transfer: Key Differences and Similarities

While ACH transfers and wire transfers both involve the electronic movement of funds, there are key differences between the two methods.

Speed: One of the main differences between Automated Clearing House (ACH) transfers and wire transfers is the speed of the transaction. ACH transfers typically take one to two business days to complete, while wire transfers are usually processed within a few hours or even minutes.

Cost: ACH transfers are generally more cost-effective than wire transfers. Many banks offer ACH transfers free of charge, while wire transfers often come with fees ranging from $20 to $50 per transaction.

Security: Both Automated Clearing House (ACH) transfers and wire transfers are considered secure methods of payment. However, wire transfers are often perceived as more secure due to their faster processing times and the fact that they are typically used for larger transactions.

International Transfers: Wire transfers are commonly used for international transactions, as they allow for the transfer of funds across different countries and currencies. ACH transfers, on the other hand, are primarily used for domestic transactions within the United States.

Benefits of ACH Transfers: Why Choose this Payment Method?

ACH transfers offer numerous benefits for individuals and businesses alike. Let’s explore some of the key advantages of using this payment method.

Convenience: ACH transfers provide a convenient way to send and receive funds electronically. With just a few clicks, individuals can initiate transfers from the comfort of their homes or offices, eliminating the need for paper checks or physical visits to the bank.

Cost-Effectiveness: Automated Clearing House (ACH) transfers are often more cost-effective than other payment methods. Many banks offer ACH transfers free of charge, making them an attractive option for businesses that need to make frequent payments or individuals who want to avoid transaction fees.

Automation and Efficiency: ACH transfers can be automated, allowing businesses to streamline their payment processes. This automation reduces the need for manual intervention, saving time and reducing the risk of errors.

Security: Automated Clearing House (ACH) transfers are considered secure, with multiple layers of protection in place to safeguard sensitive information and prevent fraud. Banks and financial institutions employ encryption and authentication measures to ensure the security of ACH transactions.

ACH Transfer Limits and Fees: What You Need to Know

While ACH transfers are generally cost-effective, it is important to be aware of any potential limits and fees associated with this payment method.

Transfer Limits: Most banks impose limits on the amount that can be transferred through ACH. These limits can vary depending on the bank and the type of account. For personal accounts, the limit is typically around $25,000 per day, while business accounts may have higher limits.

Fees: Many banks offer Automated Clearing House (ACH) transfers free of charge, especially for personal accounts. However, some banks may impose fees for certain types of ACH transfers, such as expedited or same-day transfers. It is important to check with your bank to understand their specific fee structure.

Setting Up an ACH Transfer: A Step-by-Step Guide

Setting up an ACH transfer is a straightforward process that can be done through various channels, including online banking platforms and mobile applications. Here is a step-by-step guide to help you navigate the process.

Step 1: Gather the necessary information

Before initiating an Automated Clearing House (ACH) transfer, you will need to gather the recipient’s bank account number and routing number. This information can usually be found on a check or obtained directly from the recipient’s bank.

Step 2: Log in to your online banking platform

Access your online banking platform using your username and password. If you do not have an online banking account, you may need to enroll in online banking before proceeding.

Step 3: Navigate to the transfer section

Once logged in, navigate to the transfer section of your online banking platform. This section may be labeled differently depending on your bank, but it is typically found under the “Payments” or “Transfers” tab.

Step 4: Enter the recipient’s information

Enter the recipient’s bank account number, routing number, and the amount you wish to transfer. Double-check the information to ensure its accuracy, as errors can result in failed or delayed transfers.

Step 5: Review and confirm the transfer

Review the details of the transfer, including the recipient’s information and the amount to be transferred. If everything looks correct, confirm the transfer and submit the request.

A Closer Look at ACH Transfer Security Measures

Security is a top priority when it comes to ACH transfers. Banks and financial institutions have implemented various security measures to protect sensitive information and prevent fraudulent activities. Let’s take a closer look at some of these security measures.

Encryption: ACH transfers utilize encryption technology to protect data during transmission. Encryption converts sensitive information into a code that can only be deciphered by authorized parties, ensuring that it remains secure and confidential.

Authentication: Banks employ authentication measures to verify the identity of users initiating Automated Clearing House (ACH) transfers. This can include the use of usernames, passwords, and additional security measures such as two-factor authentication or biometric verification.

Fraud Detection and Prevention: Banks have sophisticated systems in place to detect and prevent fraudulent activities related to ACH transfers. These systems analyze transaction patterns, monitor for suspicious activity, and employ artificial intelligence algorithms to identify potential fraud.

Secure Networks: Financial institutions ensure that their networks are secure and protected from unauthorized access. They employ firewalls, intrusion detection systems, and other security measures to safeguard against cyber threats.

Common Issues and Troubleshooting Tips for ACH Transfers

While ACH transfers are generally reliable, there can be instances where issues arise. Here are some common issues that individuals may encounter when using Automated Clearing House (ACH) transfers, along with troubleshooting tips to help resolve them.

Delayed Transfers: ACH transfers can sometimes take longer than expected to process. If you experience a delay, it is advisable to contact your bank to inquire about the status of the transfer. They may be able to provide additional information or expedite the process if necessary.

Failed Transfers: Occasionally, Automated Clearing House (ACH) transfers may fail due to incorrect or incomplete information. If a transfer fails, double-check the recipient’s account and routing numbers to ensure their accuracy. If the information is correct, contact your bank for further assistance.

Insufficient Funds: If you attempt to initiate an ACH transfer but do not have sufficient funds in your account, the transfer may be rejected. To avoid this issue, ensure that you have enough funds in your account before initiating the transfer.

Technical Glitches: In rare cases, technical glitches or system outages may occur, causing ACH transfers to be delayed or disrupted. If you encounter such issues, it is best to contact your bank’s customer support for guidance and updates.

Frequently Asked Questions (FAQs)

Q1. What is the difference between ACH transfers and direct deposits?

Answer: ACH transfers and direct deposits are similar in that they both involve the electronic movement of funds. However, direct deposits are typically used for recurring payments, such as payroll or government benefits, while ACH transfers can be used for various types of transactions.

Q2. Can I cancel or reverse an ACH transfer?

Answer: Once an ACH transfer has been initiated, it is generally difficult to cancel or reverse the transaction. However, if you believe there has been an error or fraudulent activity, it is important to contact your bank immediately to report the issue and seek assistance.

Q3. Are ACH transfers secure?

Answer: Yes, ACH transfers are considered secure. Banks and financial institutions employ various security measures, such as encryption, authentication, and fraud detection systems, to protect sensitive information and prevent unauthorized access.

Q4. Can I use ACH transfers for international transactions?

Answer: ACH transfers are primarily used for domestic transactions within the United States. For international transactions, wire transfers are typically the preferred method, as they allow for the transfer of funds across different countries and currencies.

Conclusion

ACH transfers have revolutionized the way we send and receive funds, providing a secure, convenient, and cost-effective alternative to traditional payment methods. Understanding the basics of ACH transfers, including how they work, their benefits, limitations, and security measures, is essential for individuals and businesses alike.

By following the step-by-step guide and being aware of common issues and troubleshooting tips, you can navigate the world of ACH transfers with confidence. Whether you are paying bills, receiving payments, or making business transactions, ACH transfers offer a reliable and efficient solution in today’s digital landscape.